How to Build a FinTech Startup: Tips From Industry Leaders

What Industry Leaders Have to Say

Building a FinTech company from scratch is a challenging venue — with many competitors and high customer expectations, 30% of entrepreneurs fail during the first two years. While it takes a lot of time and experience, at Yojji, we believe you can’t have too much information, so we’ve gathered the stories of the most successful FinTech founders with loads of experience. Keep reading to learn industry leaders’ tips and avoid similar mistakes when growing your startups.

The Rise of FinTech Startups

The market is growing annually for several reasons, including shifting consumer habits, legislative measures, and rapid technological innovation. According to Market Data Forecast, the current worldwide FinTech market value, which was approximately $111.24 billion in 2019, is expected to increase at a compound annual growth rate (CAGR) of 22.17% to reach $325.31 billion by 2026.

The evolution of technology is one factor that has largely fueled the expansion of fintechs. Businesses may now easily reach a wider audience and provide them with services that were previously only available to a select few thanks to the rise in smartphone devices and internet connectivity. Because mobile banking GIS offers accessibility, convenience, and real-time access to financial data, it is undoubtedly one of the areas that has altered how consumers handle their accounts. Another significant invention that gave rise to the notions of cryptocurrency and financial system decentralization while guaranteeing increased security and transparency is blockchain technology.

Changes in consumer attitudes were the earliest and most significant. Customers now make more digital and contactless purchases rather than in-person ones. The COVID-19 pandemic has pushed this trend even further by making it less feasible to visit physical banks and conduct currency-denominated transactions due to lockdowns and other social distancing measures. The use of digital banking and payment systems increased dramatically as a result of the epidemic, according to McKinsey & Company, and the majority of people surveyed stated that they would continue to use these services once the pandemic ended.

These domains, particularly in developing countries where financial infrastructure is still lacking, have been largely unexplored and underserved by FinTech. For instance, M-Pesa, a useful mobile payment service created by primarily unbanked individuals in Kenya, provides millions of unbanked people with access to the formal economy. It has transformed financial inclusion, lifting countless individuals out of poverty and promoting economic expansion.

The growth of Fin-tech companies has been significantly accelerated by regulation. Since governments and regulatory bodies recognize that fintech has a huge potential to advance financial services, nations all over the world have enacted legislation to encourage innovation. For instance, regulatory sandboxes enable FinTech developers to test their products in a regulatory oversight setting. This is currently evident in nations like the UK, Singapore, and Australia, all of which have made significant progress in creating an environment that is supportive of FinTech innovation.

Significant investments in the Fin-Tech sector prove this. In 2020, global fintech funding reached an astounding $44 billion, a 14% rise over the year before, according to CB Insights. Naturally, the infrequent nature of these capital infusions accounts for the Fintech companies' explosive expansion and diversification when entering new sectors. Due to their recognition of the potential of these new enterprises, venture capitalists, private equity investors, and established financial institutions started investing heavily in them.

Read also: Seven Best Conferences for FinTech Industry in 2024

Profiles of 7 Successful FinTech Founders

In addition to informing you, Yojji also wants to inspire and motivate FinTech enthusiasts, so here are seven intriguing stories that will surely make you even more passionate about new beginnings.

Chris Larsen, Co-Founder of Ripple

With the specific goal of developing a real-time payment protocol enabling safe, quick, and affordable international transactions, Chris Larsen co-founded Ripple in 2012. Despite having a background in business and having co-founded several FinTech startups, Larsen had to overcome considerable obstacles to be accepted by financial institutions and to stay under regulatory supervision. His tenacity and calculated strategy paid off, as Ripple became one of the top blockchain-based payment networks. To increase credibility and reach, Larsen highlights the significance of having a clear vision, remaining up to date on legislation, and developing strategic alliances.

With the specific goal of developing a real-time payment protocol enabling safe, quick, and affordable international transactions, Chris Larsen co-founded Ripple in 2012. Despite having a background in business and having co-founded several FinTech startups, Larsen had to overcome considerable obstacles to be accepted by financial institutions and to stay under regulatory supervision. His tenacity and calculated strategy paid off, as Ripple became one of the top blockchain-based payment networks. To increase credibility and reach, Larsen highlights the significance of having a clear vision, remaining up to date on legislation, and developing strategic alliances.

Aditya Ghosh, Co-Founder of BankBazaar

Aditya Ghosh, who co-founded BankBazaar in 2008, has extensive experience in business strategy and operations. His goal was to streamline financial product online application processes. His early days were difficult since he had to educate them about online financial services and earn their trust. BankBazaar is the top online financial marketplace in India thanks to its easy-to-use interface and thorough product comparisons. Ghosh's key recommendations for any prospective FinTech business owner are to: Educate customers; establish credibility by offering dependable and transparent services; and offer an easy-to-use platform.

Aditya Ghosh, who co-founded BankBazaar in 2008, has extensive experience in business strategy and operations. His goal was to streamline financial product online application processes. His early days were difficult since he had to educate them about online financial services and earn their trust. BankBazaar is the top online financial marketplace in India thanks to its easy-to-use interface and thorough product comparisons. Ghosh's key recommendations for any prospective FinTech business owner are to: Educate customers; establish credibility by offering dependable and transparent services; and offer an easy-to-use platform.

Taavet Hinrikus, Co-Founder of Wise (formerly TransferWise)

Taavet Hinrikus, an IT specialist and the original Skype employee, launched Wise in 2011 to provide a transparent and reasonably priced method of sending money abroad. Wise first entered a direct rivalry with well-established banks in an attempt to win over new clients, but it was his open pricing strategy—which involved far reduced fees—that started the company to take off. The major participant in the global money-transfer market these days is Wise. Openness, reasonable prices, and a steady flow of client feedback are values that Hinrikus upholds to improve its services.

Taavet Hinrikus, an IT specialist and the original Skype employee, launched Wise in 2011 to provide a transparent and reasonably priced method of sending money abroad. Wise first entered a direct rivalry with well-established banks in an attempt to win over new clients, but it was his open pricing strategy—which involved far reduced fees—that started the company to take off. The major participant in the global money-transfer market these days is Wise. Openness, reasonable prices, and a steady flow of client feedback are values that Hinrikus upholds to improve its services.

Renaud Laplanche, Founder of LendingClub

LendingClub was founded in 2007 by Renaud Laplanche, a serial entrepreneur with a background in both business and law. He sought to fundamentally change the current loan structure through peer-to-peer lending. Because of Laplanche's dedication to developing a more transparent and open lending platform despite regulatory obstacles and mistrust from traditional lenders, the company would be able to position itself as the leader in alternative financing. He advises looking for methods to disrupt established markets while, of course, adhering to legal requirements and focusing on the needs of the consumer.

LendingClub was founded in 2007 by Renaud Laplanche, a serial entrepreneur with a background in both business and law. He sought to fundamentally change the current loan structure through peer-to-peer lending. Because of Laplanche's dedication to developing a more transparent and open lending platform despite regulatory obstacles and mistrust from traditional lenders, the company would be able to position itself as the leader in alternative financing. He advises looking for methods to disrupt established markets while, of course, adhering to legal requirements and focusing on the needs of the consumer.

Anne Boden, Founder of Starling Bank

In 2014, Anne Boden, who has over 30 years of experience in banking and technology, established Starling Bank. Her objective was to make this bank a digitally first organization that places a high value on offering its customers a unique banking experience. Potential investors and well-known rivals pose a threat to Boden. However, the banks' unrivaled customer service and technology-based approach to service delivery proved crucial in Starling Bank's ascent to prominence as one of the UK's main challenger banks. Boden has some advice for aspiring FinTech entrepreneurs: prioritize customer service, use technology to innovate, and persevere in the face of hardship.

In 2014, Anne Boden, who has over 30 years of experience in banking and technology, established Starling Bank. Her objective was to make this bank a digitally first organization that places a high value on offering its customers a unique banking experience. Potential investors and well-known rivals pose a threat to Boden. However, the banks' unrivaled customer service and technology-based approach to service delivery proved crucial in Starling Bank's ascent to prominence as one of the UK's main challenger banks. Boden has some advice for aspiring FinTech entrepreneurs: prioritize customer service, use technology to innovate, and persevere in the face of hardship.

Jack Dorsey, Co-Founder of Square

Square was started in 2009 by Jack Dorsey, the man behind Twitter, to let small businesses accept credit cards. Despite issues with merchant acceptance and government taxes, Square is a major FinTech company in the payment and financial services industry. Because it offers a simple, uncomplicated, and reasonably priced solution, many customers are using it. Among Dorsey's most significant concepts are user-friendly solutions to address issues that individuals encounter, low-cost options to draw in small businesses, and scalable solutions that expand with users.

Square was started in 2009 by Jack Dorsey, the man behind Twitter, to let small businesses accept credit cards. Despite issues with merchant acceptance and government taxes, Square is a major FinTech company in the payment and financial services industry. Because it offers a simple, uncomplicated, and reasonably priced solution, many customers are using it. Among Dorsey's most significant concepts are user-friendly solutions to address issues that individuals encounter, low-cost options to draw in small businesses, and scalable solutions that expand with users.

Patrick Collison, Co-Founder of Stripe

Co-founding Stripe in 2010 to alleviate developers of the burden of online payments, Patrick Collison has a background in both computer science and entrepreneurship. At first, it was difficult to get engineers and businesses to accept you in the competitive field. Stripe is one of the biggest and most well-known payment processing firms in the world today because it offers developers a sophisticated yet incredibly user-friendly platform. Collison advises focusing on the development, adding features and developing them regularly in response to user requests while building trust by offering secure and reliable services.

Co-founding Stripe in 2010 to alleviate developers of the burden of online payments, Patrick Collison has a background in both computer science and entrepreneurship. At first, it was difficult to get engineers and businesses to accept you in the competitive field. Stripe is one of the biggest and most well-known payment processing firms in the world today because it offers developers a sophisticated yet incredibly user-friendly platform. Collison advises focusing on the development, adding features and developing them regularly in response to user requests while building trust by offering secure and reliable services.

Practical Tips for Aspiring FinTech Entrepreneurs

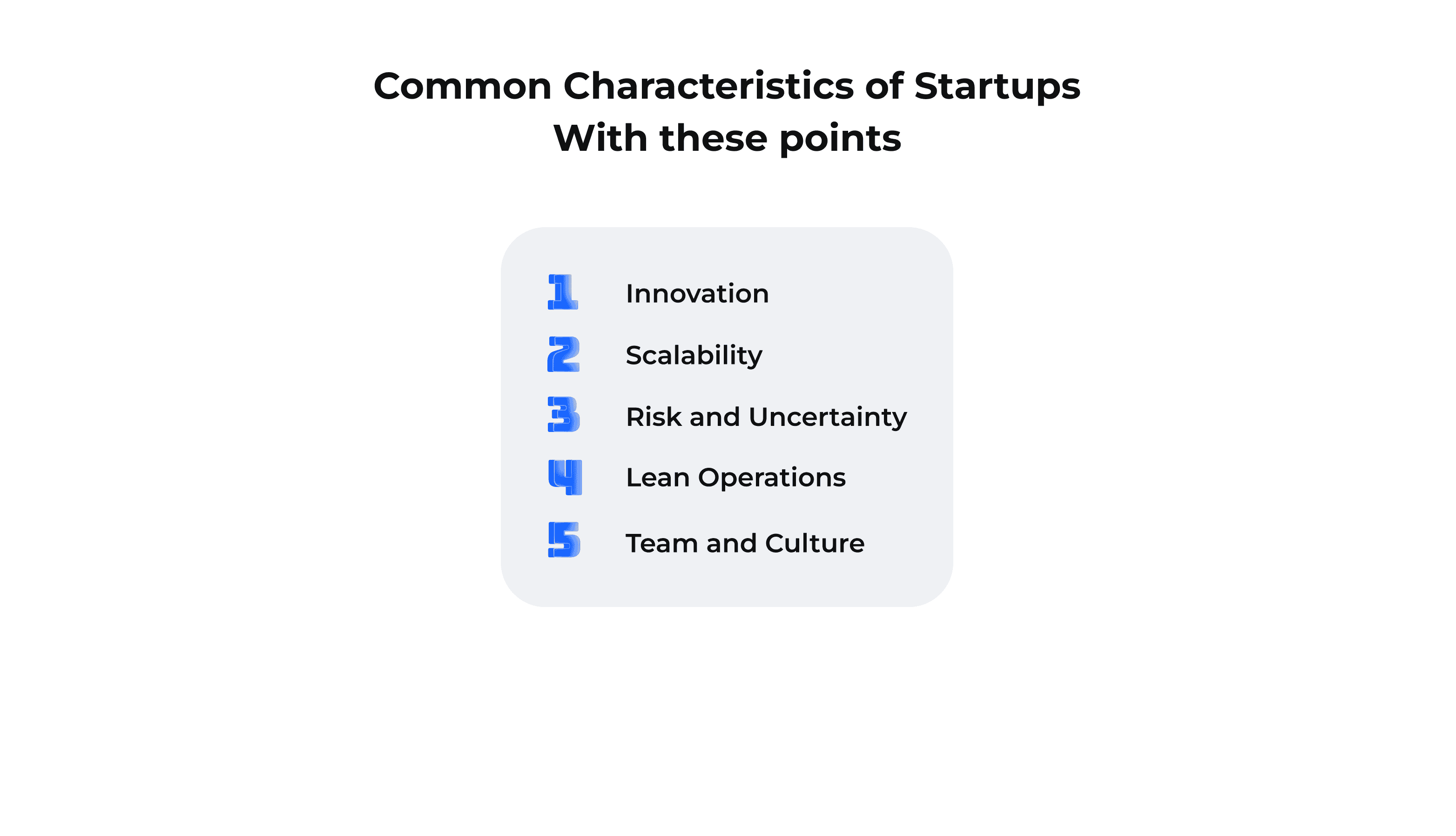

While entering the FinTech industry might be challenging, prospective FinTech companies can thrive in this competitive market by adopting the right approach. Here are five helpful guidelines to get you started:

While entering the FinTech industry might be challenging, prospective FinTech companies can thrive in this competitive market by adopting the right approach. Here are five helpful guidelines to get you started:

1. Establish a clear mission and vision first.

A well-defined goal and mission are essential when launching a financial business. Clearly state the issue you want to tackle and explain how your solution will be unique in the marketplace. A clear mission statement will direct your choices and keep your attention on your objectives. For instance, Taavet Hinrikus and Kristo Käärmann's success was primarily attributed to the low-cost, transparent international money transfers they offered when they created Wise (previously TransferWise).

2. Recognize the environment of regulations

Managing the regulatory environment is one of the main FinTech issues. Keep up with pertinent rules and make sure your company abides by them. Early interaction with regulators and legal counsel can help avoid expensive legal problems. Chris Larsen from Ripple emphasizes the significance of being aware of regulations and proactively interacting with them.

3. Concentrate on forming a robust team

Your most valuable resource is your team. Put together a team with technology, finance, marketing, and compliance expertise. Powerful team members break down obstacles, promote innovative solutions, and assure operational excellence. The major part of Anne Boden's success at Starling Bank may be attributed to the diverse and brilliant team she brought around her.

4. Use Technology to Spark Original Thought

Technology is at the heart of FinTech by nature. You may respond to your clients' evolving needs by using cutting-edge technology to create innovative solutions. The secret is to keep up with developments in everything from blockchain and artificial intelligence to smartphones. Stripe's Patrick Collison created a developer-friendly framework that streamlines online payments by utilizing cutting-edge technologies.

5. Give the user experience priority

Your FinTech solution can stand out if the user experience is smooth and simple. Perform in-depth user research and keep improving your product in response to feedback. According to data, 80% of consumers are willing to spend extra for a better user experience. Taavet Hinrikus of Wise emphasizes the significance of user-centric design in developing products that offer an exceptional user experience and effectively address real-world issues.

Keeping your end-user in mind is one of the core strategies when growing your FinTech startup. Put yourself in their shoes and use the product you’ve built — you’ll be impressed by how much you can learn.

Conclusion

A novel piece of advice for prospective FinTech business owners is to begin with a narrowly defined niche. Rather than attempting to address every financial issue at once, pinpoint a particular issue or underrepresented market area and excel at filling it. If you struggle to begin or need a trusted software development partner by your side — contact Yojj. We’re an experienced provider of tech solutions for businesses from multiple industries.

Looking to hire developers?